https://doi.org/10.1140/epjb/s10051-023-00628-6

Regular Article - Statistical and Nonlinear Physics

Analyzing volatility patterns in the Chinese stock market using partial mutual information-based distances

1

Faculty of Economic and Business Administration, Yibin University, Yibin, China

2

School of Economics and Management, Nanjing University of Science and Technology, 210094, Nanjing, China

3

Department of Occupational Health and Safety, Middle East Technical University, Ankara, Turkey

a

arashsioofy@yibinu.edu.cn

b

2021010052@yibinu.edu.cn

Received:

3

October

2023

Accepted:

22

November

2023

Published online:

19

December

2023

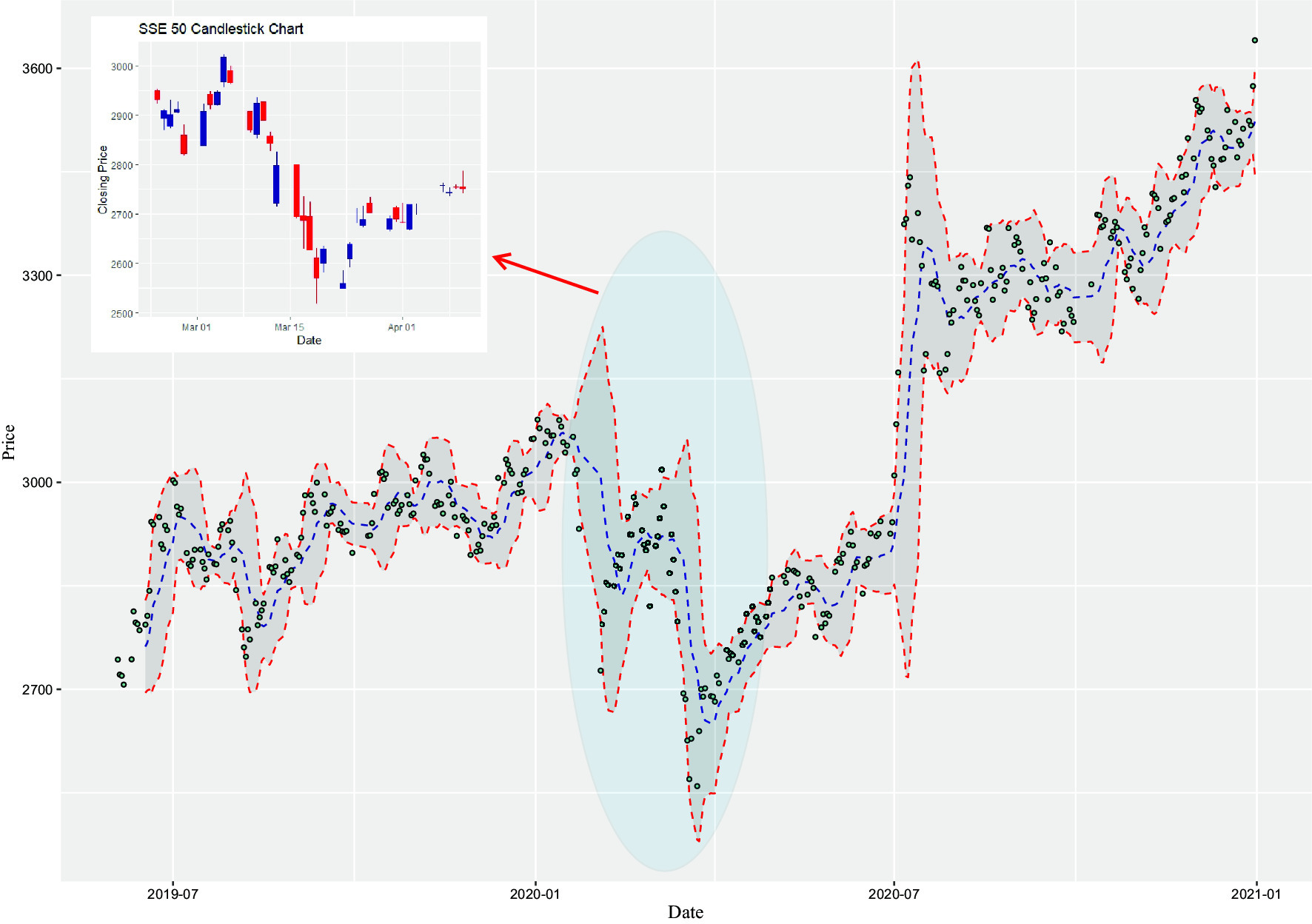

This study examines the dynamic range of financial networks in the Chinese stock market between 2019 and 2021. It provides an objective assessment of the network’s characteristics and scalability. The research time-frame is divided into three segments, reflecting the fluctuations of the financial market, including stable, volatile, and follow-up periods. To establish correlations among companies, the study employs the partial mutual information distance (PMID) method, followed by the construction of three minimum spanning tree (MST) networks for each period. Given the non-linear nature of financial phenomena, PMID is found to be more appropriate than linear methods in the study of financial markets. Additionally, the power law is observed in all three networks. This study is organized hierarchically into levels of nodes, clusters, and global indicators, providing a comprehensive perspective on network behavior and adaptation. Three-level indicators are calculated for each of the three networks, and the findings display a noteworthy variation between the volatile network and the other two networks. During stable and follow-up periods, a node-level analysis has indicated strong interconnectedness among companies. In contrast, during volatility, there are dynamic fluctuations in network dynamics. Cluster-level analysis reveals that firms become more essential connectors and actively engaged, with increased centrality. A global analysis shows that companies are more likely to form partnerships with counterparts possessing similar degrees during times of market volatility compared to periods of stability or follow-up periods. To assess the resilience of the constructed networks, we employed Markov chain analysis and examined the maximal connected component (MCC); the study findings suggest that the network is more susceptible to volatility in the observed second period, while demonstrating greater resilience in the follow-up period indicating recovery of financial markets.

Copyright comment Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

© The Author(s), under exclusive licence to EDP Sciences, SIF and Springer-Verlag GmbH Germany, part of Springer Nature 2023. Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.